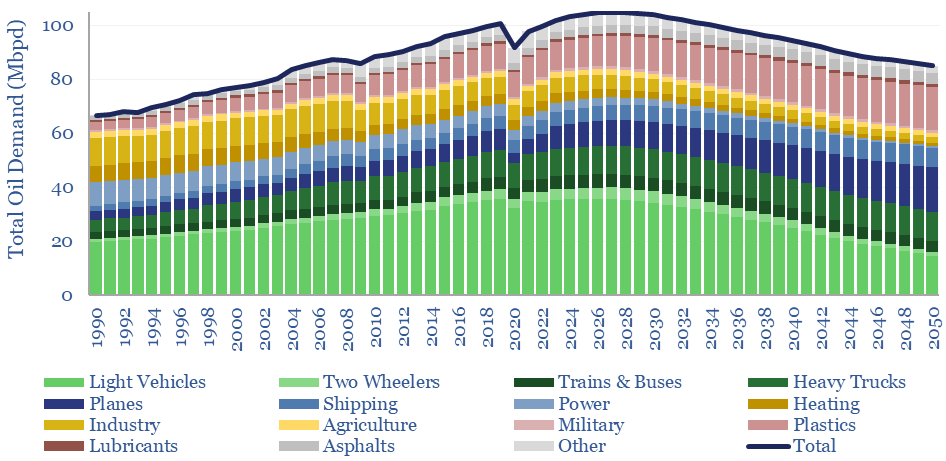

Oil’s role as a cornerstone of industrial growth and global transportation remains firmly entrenched, but predictions about its future trajectory are more divided than ever. According to the latest analysis from a leading industry coalition, the world is not anticipating a slowdown in usage any time soon. In fact, global requirements for this foundational fuel are projected to keep climbing, approaching a staggering 123 million barrels per day by the middle of this century. This outlook is built on persistent economic expansion in major developing regions and ongoing demand from sectors such as transportation, aviation, and petrochemicals. Despite recent slowdowns in key markets and strides in electrification, the fundamental forces propelling consumption, particularly in fast-growing economies, appear undiminished.

A central theme in this outlook is the rapid economic transformation taking place across South Asia, the Middle East, and parts of Africa. As incomes rise and urbanization advances, population-driven energy needs continue to intensify. Modern mobility, logistics, aviation, and chemical industries rely heavily on hydrocarbon-based fuels, with few immediate alternatives matching oil’s versatility and density. One pivotal insight from the latest report is the outsized contribution expected from India and neighboring nations; these areas alone are seen as adding millions of additional barrels in daily requirements by 2050. Alongside them, the Middle East’s industrial ambitions and Africa’s demographic boom are forecast to make these regions key drivers in the global market’s evolution.

Notably, this vision stands in contrast to analyses from several international energy authorities and independent observers. Some experts assert that shifting policies, technological breakthroughs in renewable generation, and the rapid rollout of cleaner vehicles—particularly in China and advanced economies—could change the equation far sooner. Citing evidence of a plateau in major industrialized markets and the acceleration of energy transitions that favor alternative power sources, these perspectives point to a possible high-water mark in usage within this decade. They project that global demand may crest around 2029, followed by a gradual reduction as efficiency improvements and electrification come to dominate growth pathways. The divergence in forecasts reveals deep uncertainty around the pace of innovation, the arc of policy, and the resilience of traditional consumption patterns.

The debate centers not only on the scale of future consumption but also on what will shape the energy mix itself. While hydrocarbons have underpinned global prosperity for generations, the emerging consensus is that access to secure, affordable, and sustainable energy requires significant diversification. Industry leaders stress the complexity of large-scale electrification, talking frankly about the infrastructure, cost, and policy hurdles involved, especially in regions still working to bring reliable energy to underserved communities. Yet the momentum of renewables, digitalization, and energy storage technologies may accelerate the adoption of alternatives and push the world toward a very different energy landscape.

Policy recalibration is another crucial driver. Governments that had previously committed to aggressive decarbonization goals are now also weighing priorities such as affordability and supply security, especially against the backdrop of global economic turbulence and persistent geopolitical uncertainty. Recent developments reveal that even modest adjustments in policy stance can meaningfully alter demand projections over the long term. Key stakeholders are closely monitoring developments in legislative targets, international accords, and the broader macroeconomic environment, recognizing that subtle changes can have outsized effects on investment strategies and market stability.

At the same time, the interdependence between technological progress and market evolution cannot be understated. Advances in battery technology, grid management, hydrogen production, and energy efficiency may incrementally, or abruptly, transform consumption patterns in ways that are difficult to fully anticipate. This intersection of policy and innovation will remain a defining feature of the decades ahead, underscoring the need for flexible, adaptive strategies across the entire energy value chain.

The clash between bullish and cautious projections for hydrocarbon demand reveals just how dynamic the conversation has become. On one side, scenarios suggest ongoing robust usage amid global development and persistent industrial requirements. On the other, a swift uptake of alternative sources, coupled with efficiency gains and evolving consumer behavior, could materially temper growth or even bring about a sustained global plateau sooner than many expect. The next few years will be pivotal as infrastructure is built, technologies commercialized, and policy frameworks tested against shifting realities.

Ultimately, the future distribution of global energy use will be determined by a nuanced blend of economic trends, regulatory shifts, capital allocation, and real-world technological progress. As the window for key investment decisions narrows, stakeholders across the spectrum are tasked with balancing immediate needs against long-term sustainability goals. Transparency, foresight, and adaptation will be essential as governments, industries, and communities navigate the competing demands of energy security, affordability, and environmental stewardship. Whatever shape the eventual path may take, it is clear that the world stands at a crossroad, with far-reaching implications for markets, prosperity, and the energy systems of tomorrow.